2026 Outlook Real Estate

Disclaimer: The information and materials prepared are for internal use only and on how the Dancap Family Investment Office (“Dancap”) views current market dynamics. Dancap does not guarantee the accuracy or completeness of the material and it is not intended in any manner to be investment, financial, legal, accounting, tax or other advice and should not be relied upon.

Dancap's Current Real Estate Strategy

June, 2026

Dancap has over 30 years of track record investing in real estate through third party funds, co-investments, and direct investments in major cities across North America. This market overview focuses on Dancap’s current real estate holdings based on type of investment and location and looks to provide an update on current market dynamics, outlook, and future risks.

The majority of the Dancap real estate portfolio is invested in B-class, US multifamily value-add properties in high-growth cities through funds and co-investments. Our real estate portfolio focuses on US multifamily value-add opportunities because of the strategy’s strong risk-adjusted returns coming from cost-effective CAPEX programs, organic rent growth, stable operating expenses, and strategic exit timing. We are a passive limited partner and target a minimum net 15% IRR and 2.0x MOIC over a five year hold for value-add opportunities. A smaller portion of our real estate portfolio holdings are invested in residential high-rise condo developments in the Greater Toronto Area, targeting a minimum net 20% IRR for new construction developments.

US Multifamily Real Estate Strategy

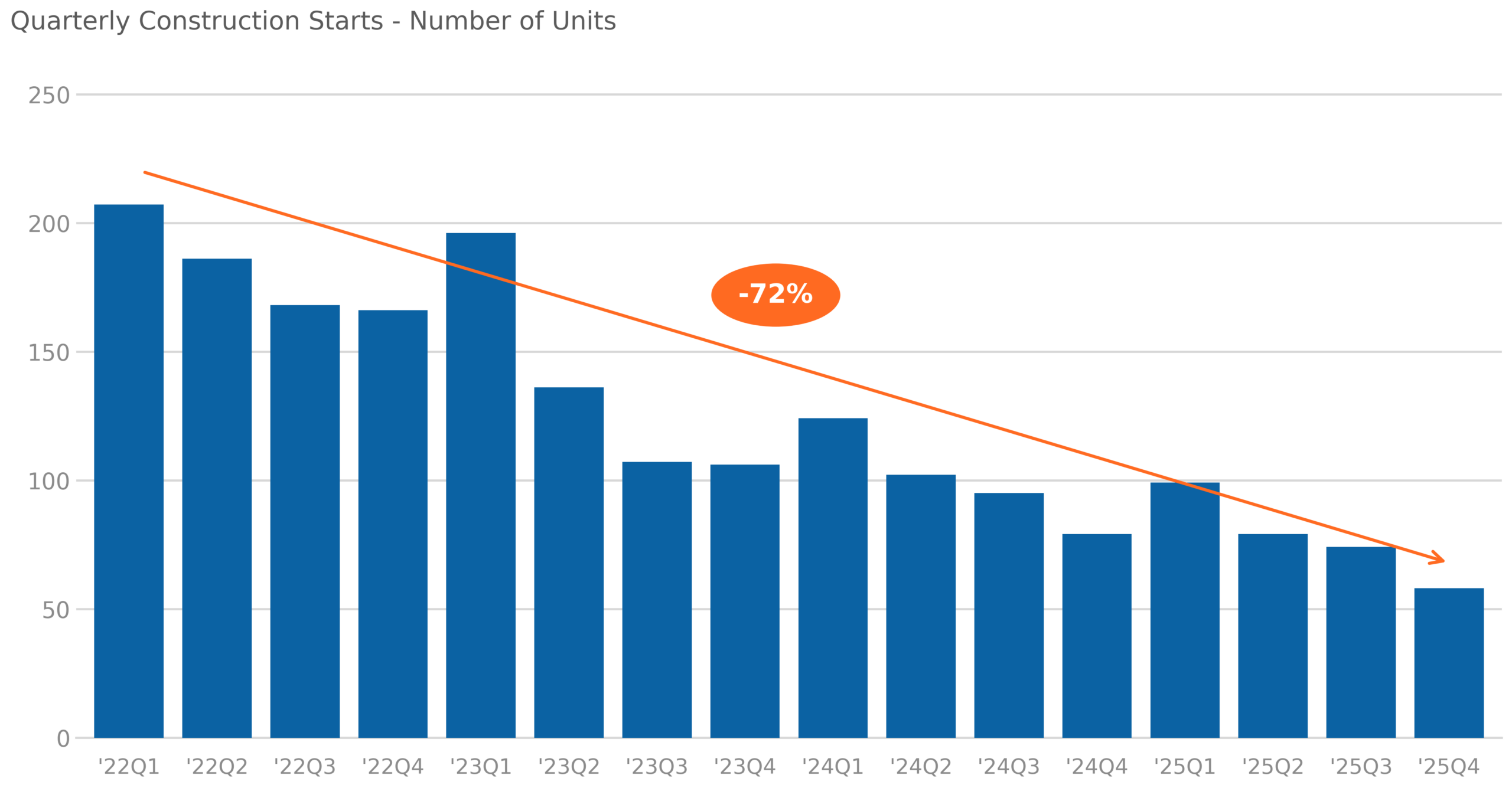

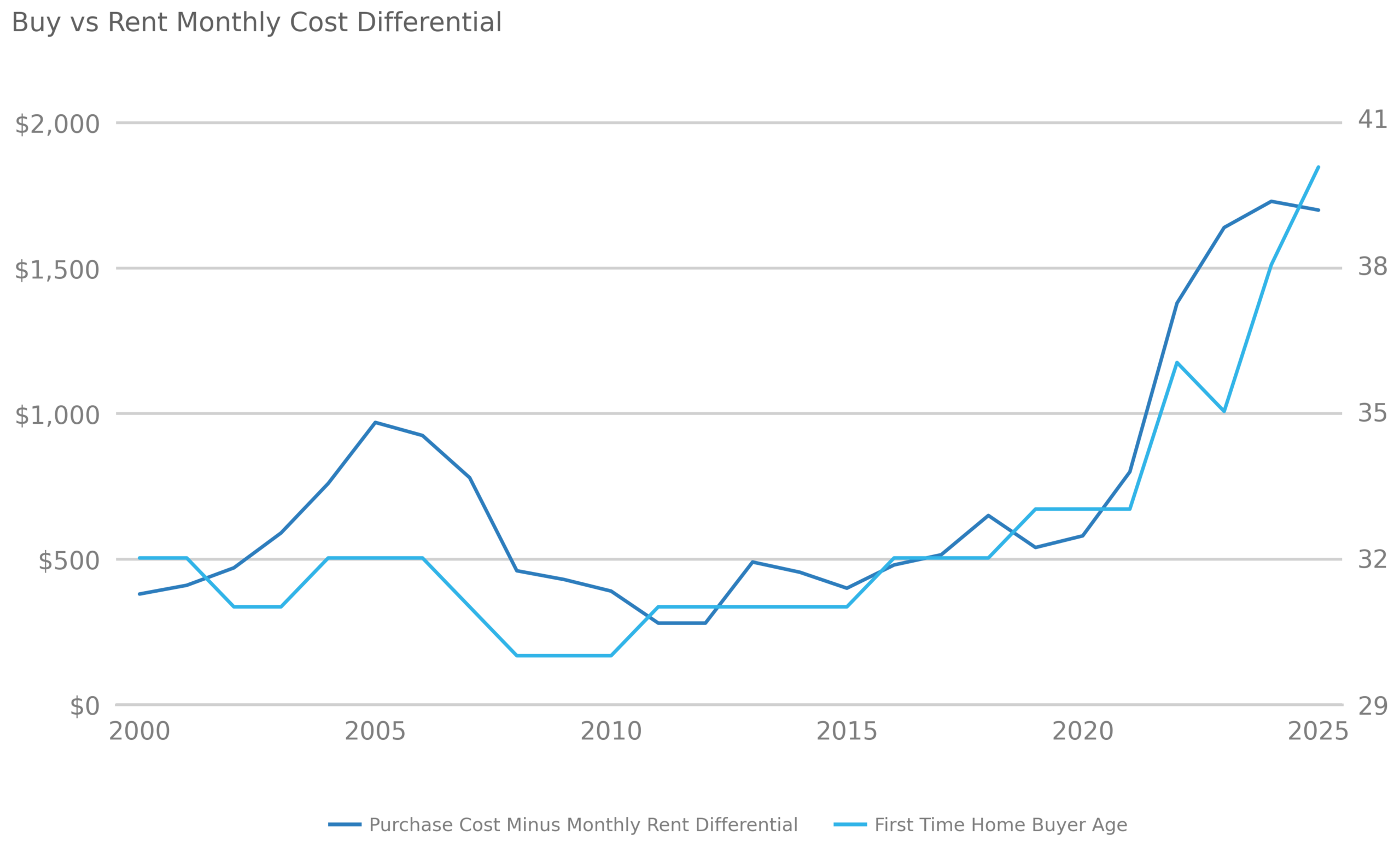

According to Morgan Stanley, U.S. multifamily supply is beginning to reset after the post-COVID construction surge. The construction starts chart shows quarterly starts falling by approximately 72% from the 2022 peak, declining from roughly 200,000 units per quarter to closer to 60,000 units by late 2025. While the recent delivery wave has pressured rents in certain markets, the pullback in new starts should reduce future supply and may support improving fundamentals as existing inventory is absorbed. This reset in supply is particularly meaningful given that construction lead times typically span 18 to 24 months, meaning the benefits of today’s reduced starts will likely begin to materialize in net operating income and occupancy metrics by 2027. At the same time, the rent-versus-own dynamic remains supportive of rental demand. The chart shows the monthly cost of owning versus renting widening materially, with the purchase cost less monthly rent differential rising to approximately $1,800 per month by 2025. This affordability gap, coupled with elevated home prices, higher mortgage rates and broader inflationary pressures, continue to make homeownership more difficult for many households.

Source: Morgan Stanley; A Cyclical Opportunity with Structural Demand Support; April 13, 2026

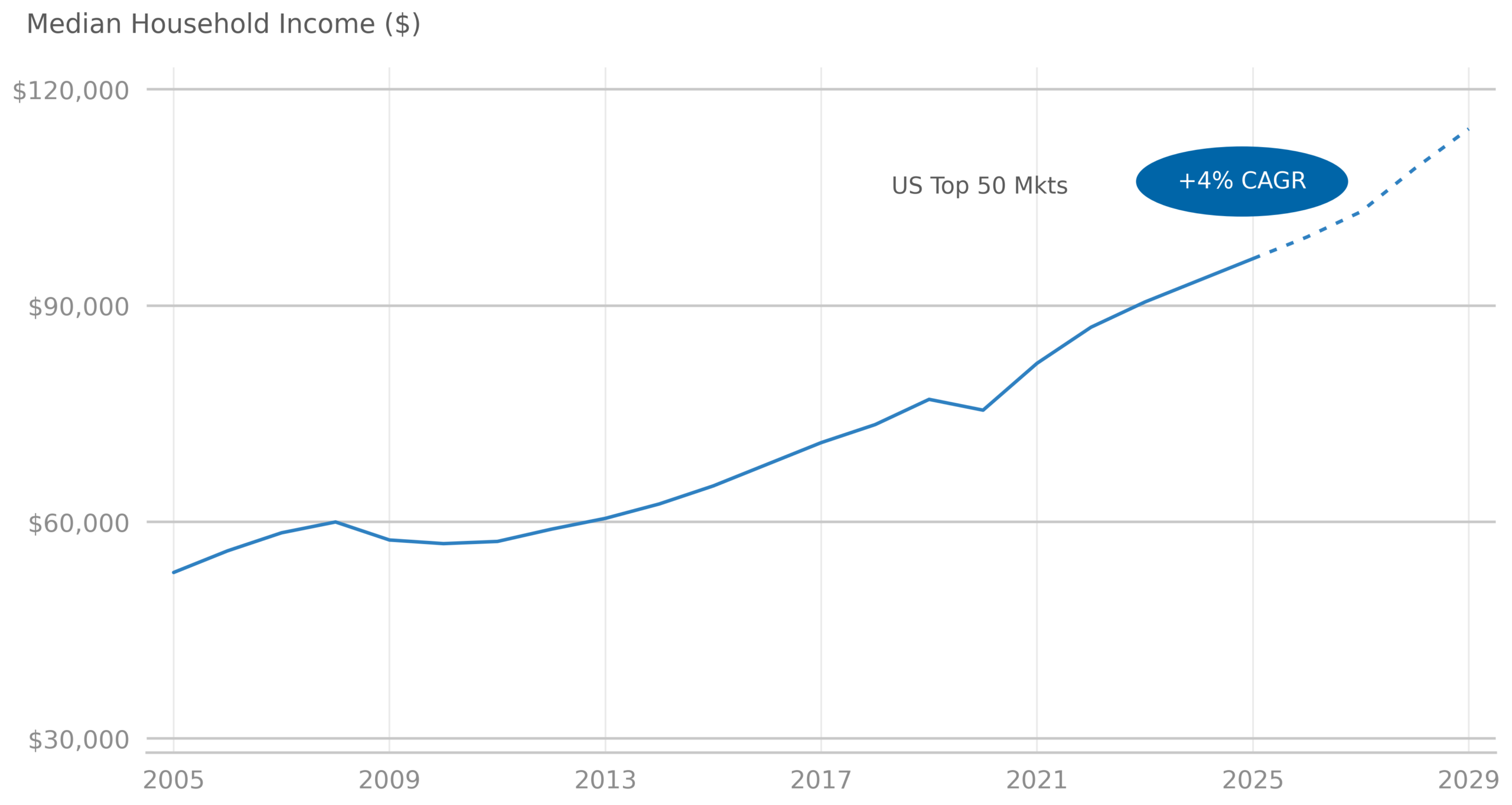

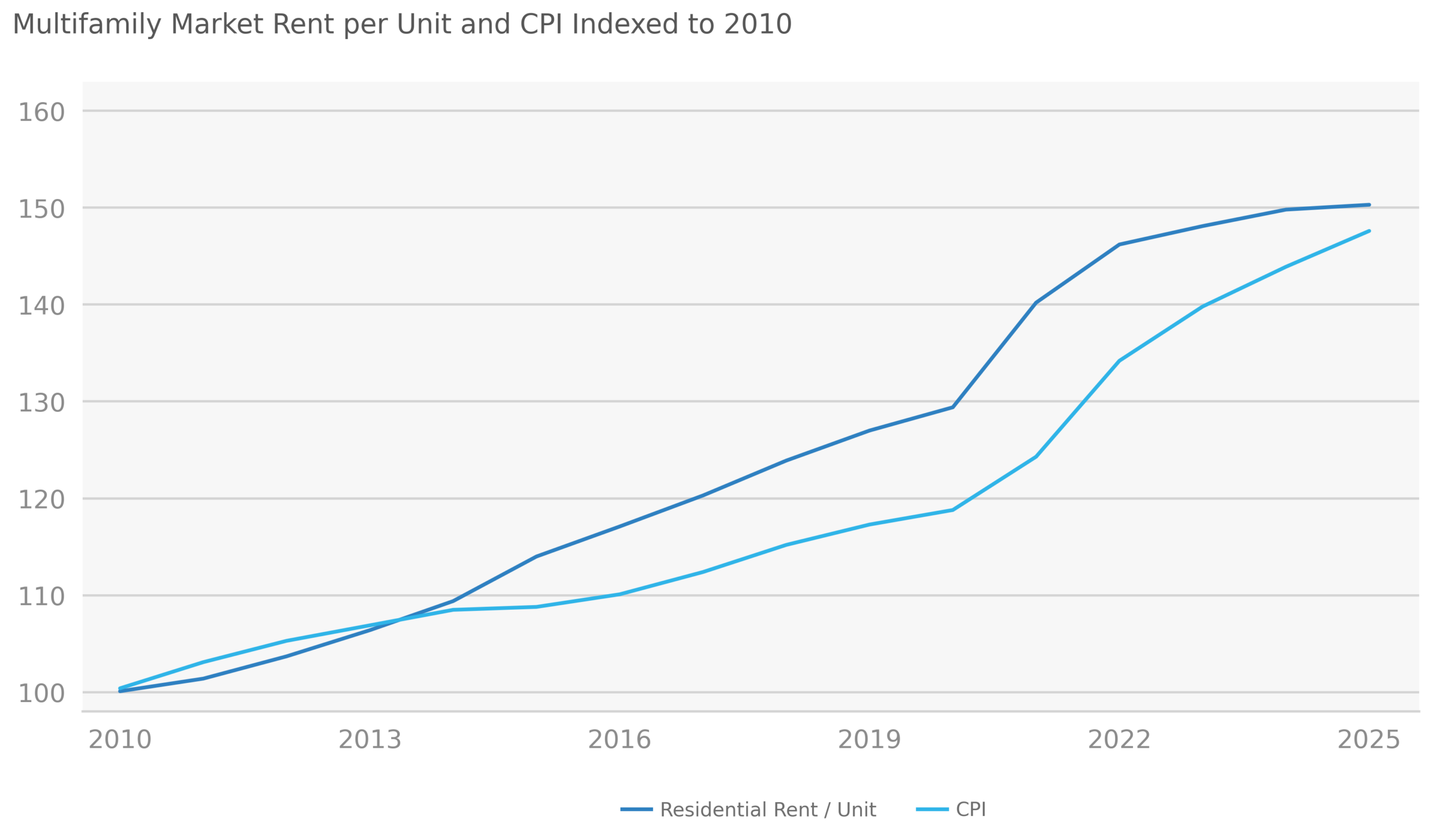

Multifamily demand is also supported by income growth and inflation-linked rent dynamics. The chart below shows median household income in the top 50 U.S. markets rising from roughly $55,000 in the mid-2000s to around $100,000 today, with Morgan Stanley forecasting approximately 4% annual growth through 2029. At the same time, multifamily market rents have increased from an index level of 100 in 2010 to roughly 150 by 2025, modestly ahead of the CPI inflatiuon index. This suggests rents have broadly kept pace with inflation while remaining supported by household income growth and the continued affordability gap between renting and owning.

Source: Morgan Stanley; A Cyclical Opportunity with Structural Demand Support; April 2026

From an investment standpoint, declining new supply, resilient renter demand and reset valuations may create a more attractive entry point. However, selectivity remains important as certain markets continue to work through excess inventory. Investors may want to focus on markets where new construction has pulled back, affordability remains constrained and valuations are compelling relative to long-term fundamental.

US Multifamily Outlook

The near-term multifamily outlook remains mixed, with softer demand and lingering supply pressure expected to keep rent growth muted through much of 2026.

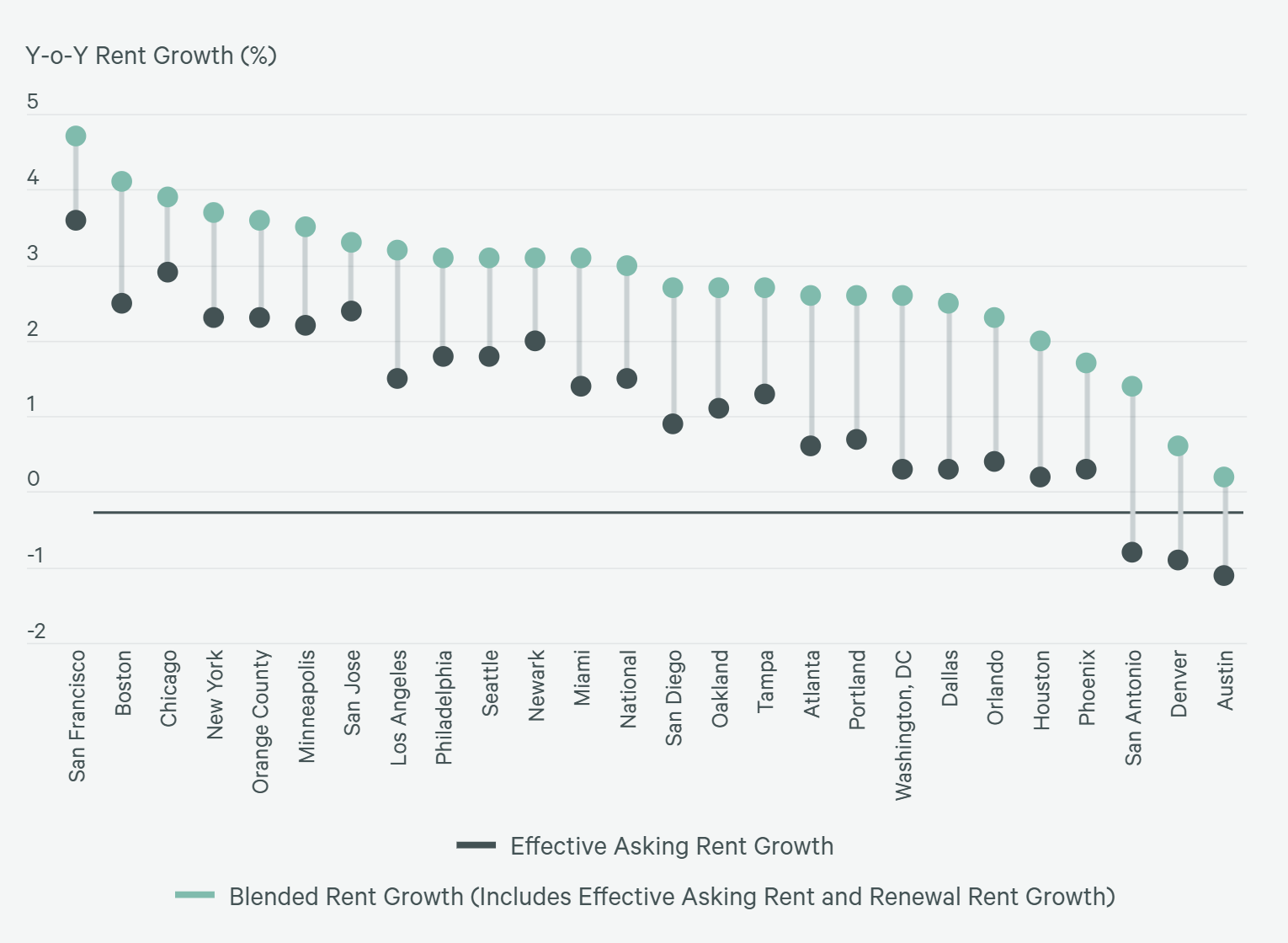

According to CBRE, vacancy rates have stabilized nationally, but rent growth is expected to remain below pre-pandemic levels in 2026 as the multifamily market continues to absorb the remaining supply pipeline. The chart below highlights this dynamic: effective asking rent growth, which reflects new lease pricing net of concessions, is expected to remain weaker than blended rent growth, which includes both new leases and renewals. This distinction matters because renewals now represent approximately 57% of all leasing activity, helping reduce turnover costs, vacancy risk and pressure from weaker new lease pricing. As a result, commonly cited asking rent growth figures may understate actual property-level performance. Blended rent growth is expected to remain higher than new lease asking rent growth in 2026, particularly in markets where concessions are still being used to preserve occupancy. For investors underwriting deals today, this distinction between blended and asking rent growth is a critical input as models that rely solely on asking rent figures risk understating stabilized cash flow, which can meaningfully affect both return assumptions and financing outcomes.

Source: CBRE U.S. Multifamily Real Estate Market Outlook 2026

Cap rates are expected to remain broadly stable in 2026, with potential for modest compression in subsequent years if interest rates and inflation remain stable, debt markets remain competitive and transaction activity continues to recover. Dancap remains selectively constructive on U.S. multifamily, with a focus on markets where new supply is declining, renter demand remains durable and valuations are compelling relative to long-term fundamentals.

Greater Toronto Area (GTA) Multifamily Strategy

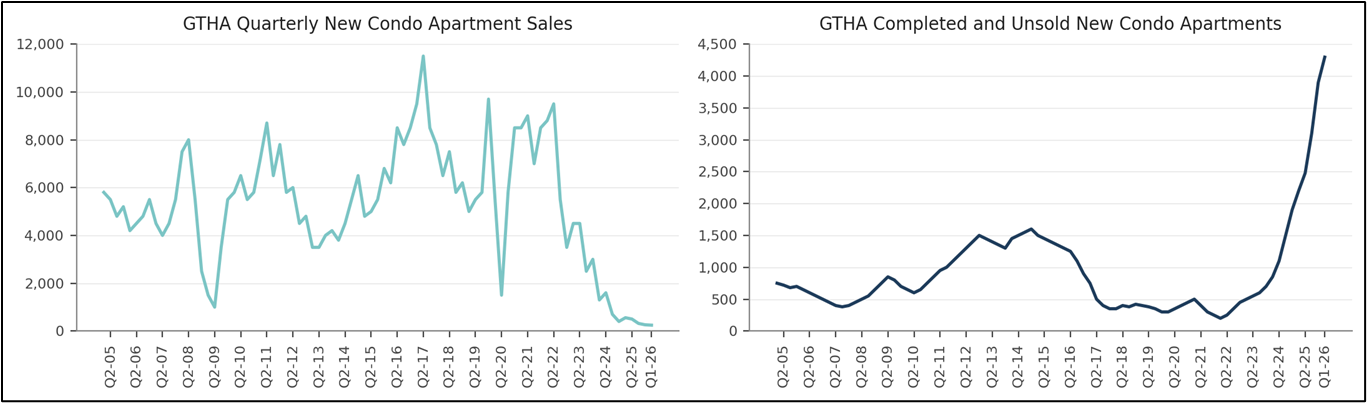

According to Urbanation, the GTA new condominium market remained under pressure in Q1 2026, with only 246 sales, 94% below the 10-year average and the lowest level in 35 years. Sales were down 6% from Q4 2025 and 52% year-over-year. Notably, there were no new project launches during the quarter, the first time this has occurred in at least 30 years. Completed but unsold new condo inventory reached a record 4,295 units, more than double the level from a year ago and nearly five times higher than two years ago. Based on the trailing 12-month sales pace, this represents 92 months of completed standing inventory. The recently announced full HST rebate, effective from April 1, 2026 to March 31, 2027, is expected to reduce new condo prices by approximately $100,000 on average, narrowing the new-versus-resale gap to roughly 20%. Developer activity also continues to weaken. In Q1 2026, 963 units were cancelled, all converting to purpose-built rental. Since the start of 2024, total cancellations have reached 11,424 units, of which 4,064 have shifted to rental, resulting in a net removal of 7,360 condo units from the future ownership pipeline.

Source: Urbanation; Standing Condo Inventory Hits Record High in Q1, April 16, 2026

Capital is starting to mobilize on the demand side. In March 2026, Toronto-based High Art Capital and the provincial Building Ontario Fund launched a $1.3B public-private fund to acquire blocks of unsold GTA condos and convert them into rental housing, with the goal of absorbing roughly one-third of the completed unsold inventory.

GTA Multifamily Outlook

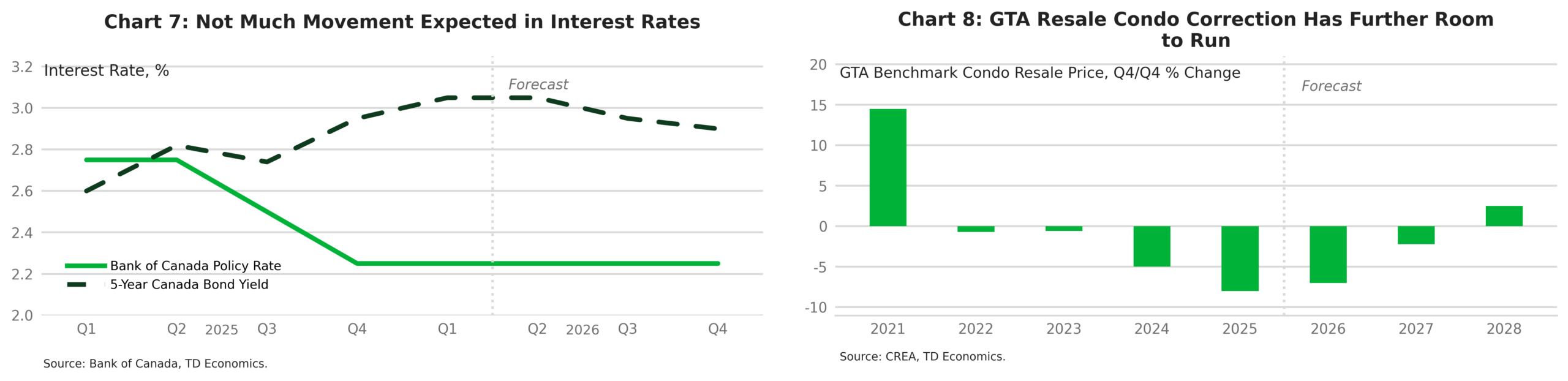

TD Bank expects the Bank of Canada to hold its policy rate at 2.25% through at least year-end 2027. Under this outlook, mortgage rates are likely to remain broadly in line with current levels, with 5-year fixed rates around 4.00% to 4.25% and only modest further declines in government bond yields, which influence fixed mortgage pricing. As a result, interest rates are unlikely to provide a meaningful tailwind to housing demand before 2028. Within the GTA condo market, TD projects continued price pressure through 2027. By that point, condo prices are expected to have declined approximately 25% to 30% from their early 2022 peak, including an additional 5% to 10% decline from Q1 2026 through the second half of 2027. A recovery is expected to begin in 2028, supported by improved affordability following the price reset and a more constrained supply backdrop.

Source: TD Bank; GTA Condo Market Outlook. May 7, 2026

Dancap remains cautiously optimistic on the GTA condo market, but believes patience and selectivity will be important as the market works through elevated supply, near-term price pressure, and higher interest rates for longer.