2026 Outlook Private Debt

Disclaimer: The information and materials prepared are for internal use only and on how the Dancap Family Investment Office (“Dancap”) views current market dynamics. Dancap does not guarantee the accuracy or completeness of the material and it is not intended in any manner to be investment, financial, legal, accounting, tax or other advice and should not be relied upon.

Dancap's Current Private Debt Strategy

June, 2026

Dancap has over 25 years of experience investing in private debt through third-party fund managers and co-investments. This market overview reflects how Dancap’s private debt portfolio is currently positioned, highlighting its alignment with our investment strategy, geographic allocation, and an analysis of prevailing market dynamics, outlook, and potential risks. The majority of Dancap’s private debt exposure is allocated to third-party managed funds that focus on U.S. senior secured, floating-rate, sponsor-backed corporate lending strategies. These strategies, with modest leverage, aim to deliver strong risk-adjusted returns, downside protection, and stable income, particularly in a rising interest rate environment.

Our private debt managers have long-standing track records across multiple market cycles and work with sponsors who bring proven expertise in their fields. Our senior secured lending strategies target minimum net returns of 10% IRR, while our second-lien and mezzanine strategies target minimum net returns of 15% IRR. This approach reflects our focus on maintaining a balanced portfolio with attractive returns and risk mitigation. Generally speaking, for private credit strategies, our preference is to invest in the senior part of the capital structure, with most of the returns coming from quarterly yield distributions.

US Private Debt Strategy

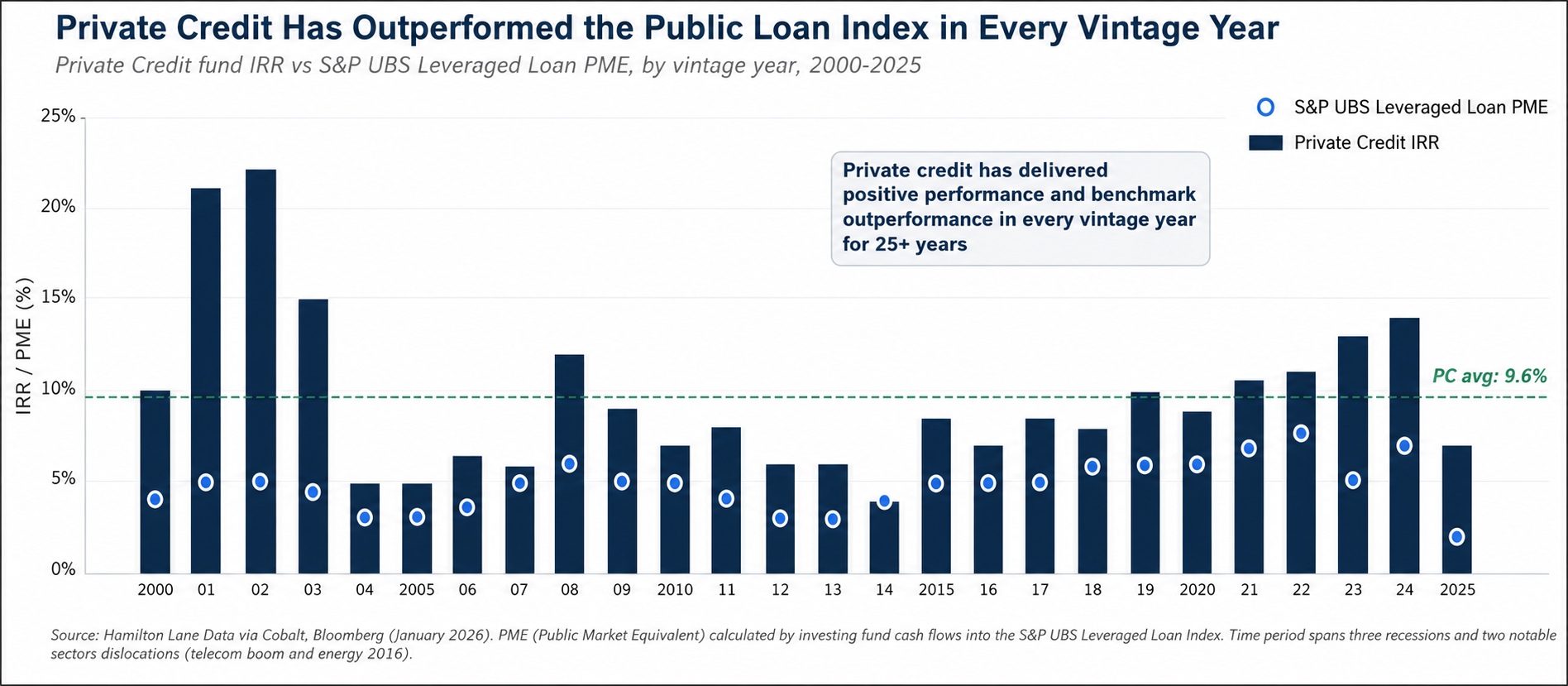

Historical returns data continues to support maintaining a dedicated allocation to private credit throughout market cycles. According to Hamilton Lane, private credit has delivered positive performance in every vintage year for the past 25 years, and has outperformed the S&P UBS Leveraged Loan Index on a Public Market Equivalent basis in every vintage year over that period. This track record spans three recessions and two notable sector-specific dislocations (telecom in 2001 and energy in 2016). Periods of volatility have historically been precisely the moments when a disciplined, long-term approach to the asset class has been rewarded, as banks tend to retrench during these episodes, making way for better pricing and structure for private credit lenders.

Source: Hamilton Lane: 2026 Credit Focus: Keeping Calm and Carrying On

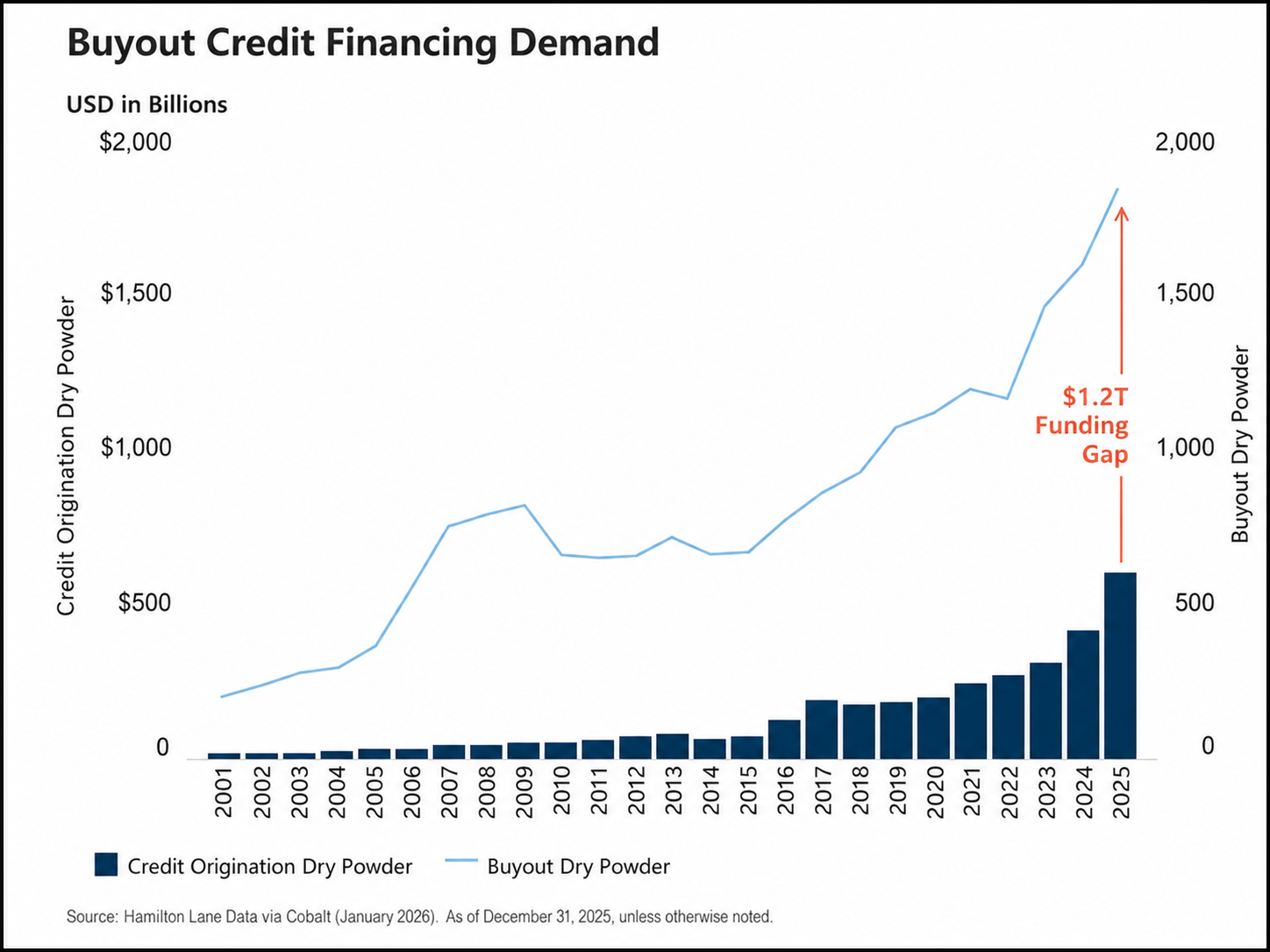

Stringent bank regulation following the 2008 Global Financial Crisis has continued to push lending activity away from traditional banks and the broadly syndicated loan market, creating a tailwind for private credit. At the same time, private equity buyout sponsors are sitting on a record $1.7 trillion of dry powder. As that capital is deployed into new acquisitions, sponsors will continue to need debt financing alongside their equity commitments, creating a significant runway for private credit lenders. Hamilton Lane’s analysis highlights the scale of that opportunity; If that $1.7 trillion of capital is deployed into buyout transactions financed with a 50% equity and 50% debt structure, it implies a need for approximately $1.7 trillion of debt financing. Against roughly $500 billion of available private credit dry powder, that leaves an estimated funding gap of $1.2 trillion.

Source: Hamilton Lane; Private Credit: Bridging Buyout’s $1.2 Trillion Funding Gap

For investors, this imbalance should create a sizeable, multi-year opportunity to deploy capital across new originations, refinancings, and sponsor-backed lending opportunities. It also reinforces the view that private credit is not an overcrowded trade. The supply of available private credit capital remains well below the financing need created by buyout dry powder and upcoming refinancing activity, leaving room for managers to put capital to work and generate meaningful returns.

US Private Debt Outlook

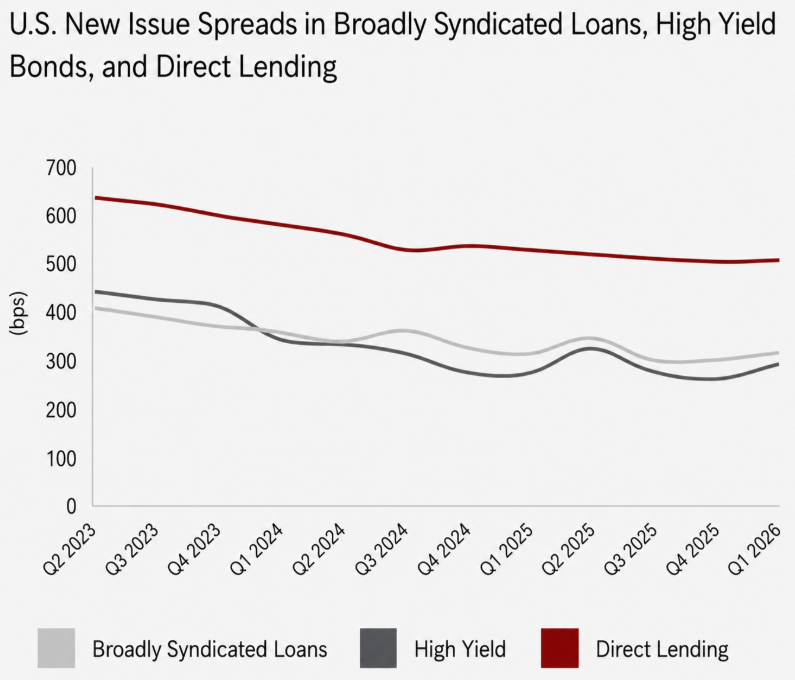

Recent volatility in the credit markets and broader risk-off sentiment has led to early signs of repricing across credits. From Q4 2025 to end of Q1 2026, new issue spreads widened modestly across broadly syndicated loans, high yield bonds, and direct lending, with public credit markets showing approximately 15 to 30 basis points of spread widening. Direct lending spreads also moved higher, but the adjustment has been more gradual, as private credit transactions already in process typically continue to close at pre-agreed terms. As of Q1 2026, direct lending new issue spreads remain close to 5.0% over SOFR, compared to approximately 3.0% for broadly syndicated loans and slightly below 3.0% for high yield bonds. That spread premium remains meaningful, particularly given that direct lending is typically senior secured and sponsor-backed.

Combining today’s base rates with current spreads, direct lending continues to offer attractive gross return potential. With the 3-month SOFR rate at approximately 3.5%, direct lending spreads of 5.0% to 6.0%, and approximately 1.0% to 1.5% of annualized discounts and upfront fees, gross annual returns for private credit loans are in the 9.0% to 11.0% range before leverage, losses, expenses, and manager fees.

Source: Northleaf Capital; Private Credit Market Update: Q1-2026

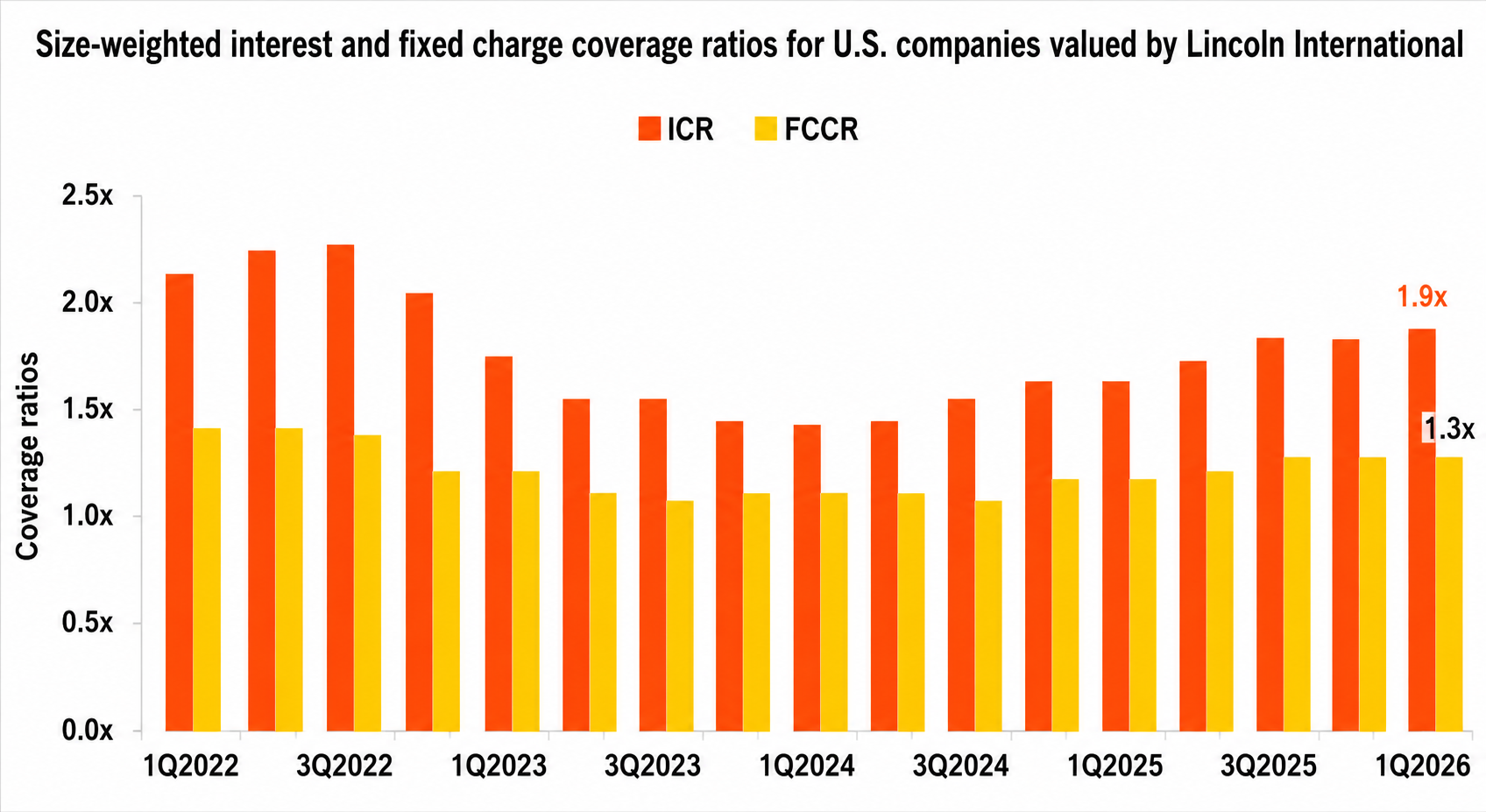

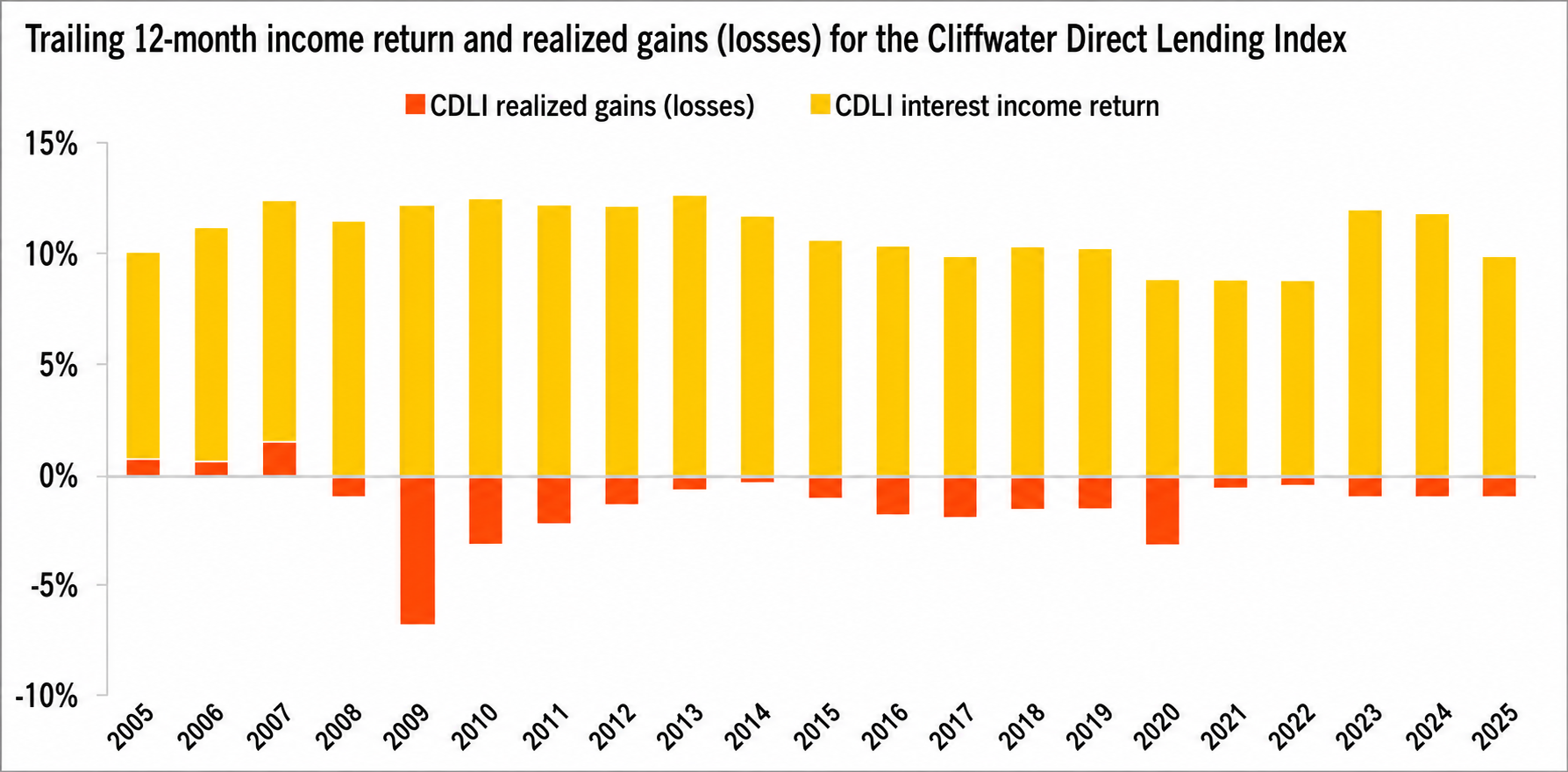

According to BlackRock, private credit fundamentals remain broadly intact even as the credit cycle matures. Borrower coverage ratios have improved meaningfully off their 2024 lows, with interest coverage (ICR) now at 1.9x and fixed charge coverage rations (FCCR) at 1.3x across the U.S. companies tracked by Lincoln International. As of Q1 2026, 63% of borrowers in the Lincoln universe are growing EBITDA year-over-year, at an average rate of 4.6%, slightly above the 10-year average of around 3%. Realized losses have stayed small relative to the income the asset class generates, with the Cliffwater Direct Lending Index showing trailing four-quarter realized losses of just 0.6%.

Source: Blackrock – Credit Currents: Insights across public and private credit

That said, BlackRock cautions that headline default numbers can be misleading on their own. Reported default rates ranged from roughly 1.1% to 5.6% across providers as of year-end 2025, depending on what is counted as a default, how the calculation is weighted, and which borrowers are included in the sample. More importantly, the gap between stronger and weaker borrowers is widening, placing a greater premium on manager selection, rigorous underwriting, and the ability to execute workouts when needed. These dynamics support Dancap’s focus on senior secured, sponsor-backed private credit strategies managed by firms with deep track records, stable teams, demonstrated underwriting discipline, and proven workout capabilities.

To see the Dancap Private Credit Investment Criteria and Portfolio, please click here.